0

Contact Us

The Government has introduced a Bill to significantly increase the penalties for breaches of the FTA. Currently, businesses can be fined up to $600,000 per contravention. The proposed amendments would see penalties for companies increase by 733% to the greater of:

The same structure for penalties applies to individuals, except with a $1 million cap (increased by 400% from $200,000).

The increased penalties will apply to all conduct occurring after the Bill comes into force, and will not have retrospective effect to conduct occurring prior to that time.

There will also be a change from a criminal liability regime to a civil regime for most breaches. This means that the Commerce Commission (as regulator of the FTA) should find it easier to prove breaches of the FTA, given that it will no longer have to establish a breach to the criminal standard of beyond reasonable doubt and will instead move forward on the civil balance of probabilities standard.

The primary driver behind these amendments is the ongoing concern of the Commerce Commission that the current penalties imposed do not eliminate the financial incentives for breaching the FTA. As such, the Commission considers they can be absorbed by non-compliant companies as a simple cost of business.

Coming out in support of the proposed changes, the Commerce Commission noted that between July 2020 and July 2025 it received more than 48,000 complaints about fair trading issues such as misleading advertising, inaccurate pricing, refund refusals, and subscription traps. This was a 23% increase to the prior period.

A secondary reason for the increase is to better align the penalty regimes in New Zealand and Australia. The proposed structure that will be adopted is closer to equivalent laws in Australia (although the Australian maximum penalties will remain much higher).[1]

There is currently a large gulf between the penalties imposed by the Courts in New Zealand and Australia for broadly similar conduct. Given the statutory maximum of $600,000 per contravention, New Zealand penalties seldom exceed a million dollars. Australia’s statutory maximum of A$50 million per contravention means that its penalties often sit in the tens of millions with the highest being a A$428 million penalty imposed against the Phoenix Institute of Australia Pty Ltd in July 2023.

However, the Government has not sought to completely align the two regimes. Following consultation with business and other groups, it was decided not to follow Australia’s lead and proceed with proposals to stop directors taking out insurance or indemnify themselves from penalties under the Act. It also opted not to progress proposals to expand infringement fees and unfair contract terms provisions.

Penalties for breaches of the FTA were last increased over a decade ago in December 2013 when they were tripled from $60,000 to $200,000 for individuals and from $200,000 to $600,000 for companies.

As those increases only applied to conduct that occurred from June 2014, it took in practice until around 2017 for the increased penalties to make an impact.

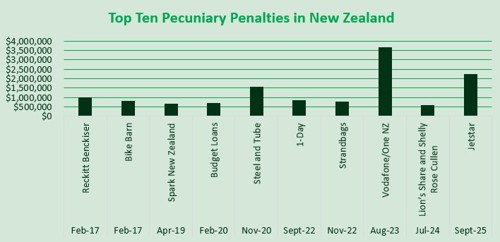

The graph below shows the ten highest pecuniary penalties imposed in New Zealand since then, which range from $600,000 to $3,675,000:

For a glimpse of the future, the fair dealing regime in the FMCA is instructive. The FMCA similarly prohibits false and misleading conduct but specifically in relation to financial products and services. The penalties for breach of the FMCA are the same as the proposed new penalties under the FTA.

While FTA penalties have only exceeded $1 million on three occasions in the last five years, in the same period FMCA penalties exceeded $1 million on 12 occasions with the highest penalty being $19.5 million.

The Bill will soon be referred to Select Committee for review, where businesses and consumers will be able to provide feedback to the proposed changes.

The changes, together with signals from the Commerce Commission that it will be a more proactive enforcer, highlight the importance of having effective compliance programmes, including training for staff. Businesses should be on notice that breaches of the FTA will continue to be an enforcement priority for the Commerce Commission and will soon attract significantly higher penalties. They should also be aware that liability for pecuniary penalties may extend to directors and senior officers.

If you want help in making a submission on the Bill, refreshing your compliance programmes or have any question about how the FTA applies to your business, please contact a member of our consumer law team.

[1] In Australia, the maximum financial penalty for breaches of fair trading laws is $A50 million, three times the benefit obtained or 30 per cent of turnover.